OIS Discounting: Changing the Way Interest Rate Swaps are Valued

Download a PDF of this white paper

What is OIS?

The acronym OIS stands for Overnight Index Swap and represents a term interest rate swap against an overnight index. In the United States, the OIS curve represents – in its most simplistic sense – the Federal Funds curve.

Figure 1 plots the Federal Funds curve against a curve that is much more familiar to many participants in the interest rate derivatives markets: the 3 Month LIBOR curve. As seen in the graph, the anticipated forward rates for Fed Funds are currently lower than those for 3 Month LIBOR. While this difference may seem rather small, it could have significant meaning for some end users of interest rate derivatives.

Figure 1: 3 Month LIBOR forward rates versus Fed Funds forward rates

Not only does OIS currently trade at a discount to 3 Month LIBOR, but it has consistently done so throughout modern history. Figure 2 shows that the difference between 3 Month LIBOR and 3 Month OIS has averaged approximately 46 basis points (0.46%) over the past 5 years and is currently only 8 basis points (0.08%) below this average.

Figure 2: 3 Month LIBOR versus 3 Month OIS over the past 5 years.

What Changes Are Occurring and Why?

Swap dealers across the industry are changing the way they discount cashflows for interest rate derivatives. For decades, dealers used the 3 Month LIBOR curve as the standard for discounting. Following the credit crisis that began in 2007, dealers felt that the value of interest rate swaps should be calculated using the same discounting methodology used to determine earnings on collateral posted against those swaps. In other words, if a dealer is posting cash as collateral for a swap and that cash is earning Fed Funds, shouldn’t the value of the swap be determined by discounting with Fed Funds?

Throughout 2012, we expect the majority of all swaps dealers to begin discounting along a term curve – OIS curve – that has historically traded at a discount to the 3 Month LIBOR curve. By using a lower discount rate, anticipated net cashflows on interest rate swaps will be valued closer to their par values and end users may be significantly impacted.

How Will OIS Discounting Impact End Users?

Dealers’ move to OIS discounting will have varying effect for end users depending upon:

The shape of the then-current yield curve

The absolute level of interest rates

The LIBOR-OIS spread for the tenor of the associated derivative

The particular derivative the end user has in place or is considering executing.

Focusing on today’s interest rate environment, the most noticeable impact to end users will be for those users that currently have swaps in place. In particular, long-term swaps that are deeply “under water” can be significantly affected.

Once a swap has been entered into, the value of that swap will be impacted by the market’s anticipation for the future path of the variable rate index(es) to which that swap is subject (i.e. – the forward curve). For the most common type of interest rate derivative implemented by end users – a swap under which the borrower pays a fixed rate and receives a variable rate – the value of the swap becomes an increasing liability as term rates decrease. Based on the current level of interest rates, many end users’ swaps have reached their highest liability since inception. When dealers convert to OIS discounting, these liabilities will grow even larger.

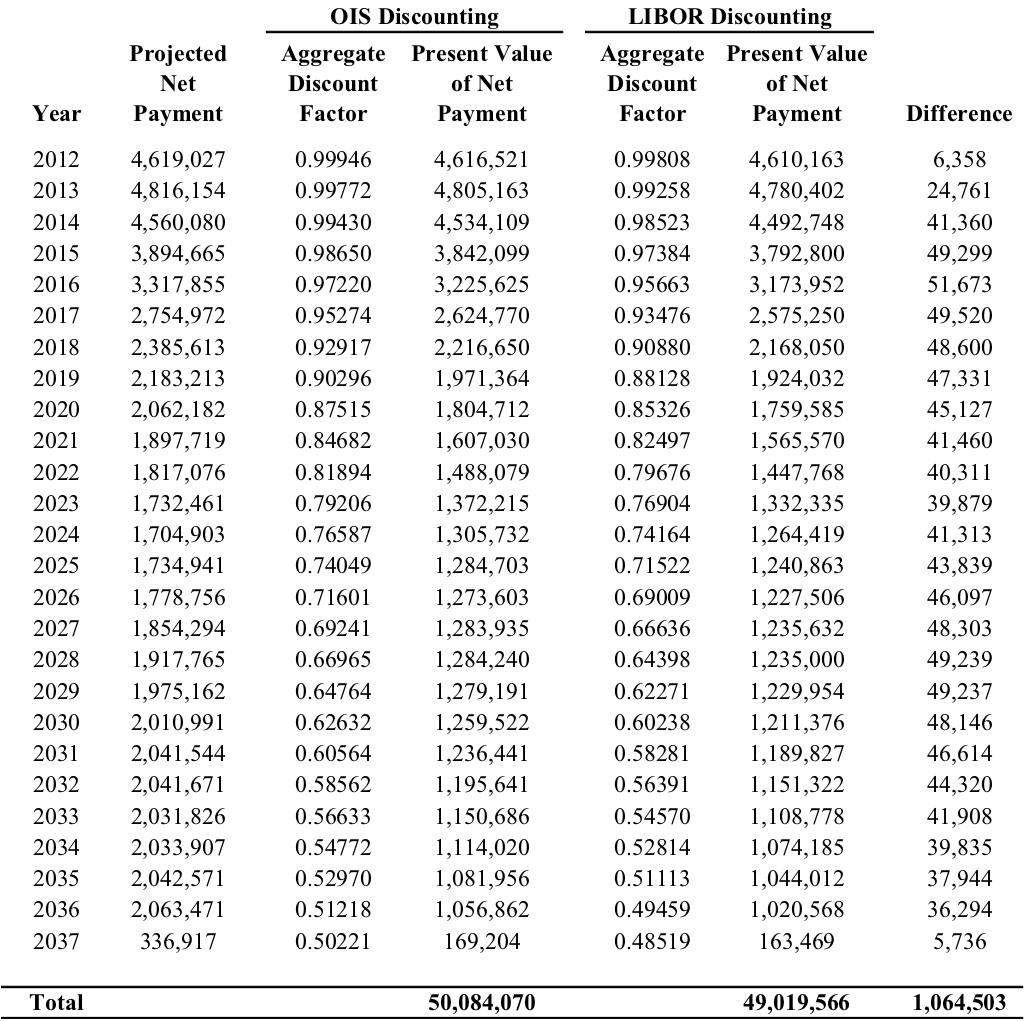

Figure 3 below outlines cashflows for a $100 million, non-amortizing swap against 1 Month LIBOR. We have assumed that this particular end user entered into a thirty year swap in February 2007 paying 5.25% and has twenty five years remaining. The projected net cashflows represent the difference between the 5.25% coupon and the currently anticipated 1 Month LIBOR forward rates. For brevity, we have aggregated cashflows and discount factors by year.

Based on the current market, converting the discount curve from 3 Month LIBOR to OIS increases the value of the swap by over $1 million to the detriment of the fixed rate payer. This change is equivalent to increasing the fixed rate on this particular swap by over 5.5 basis points (in derivatives vernacular: 5.5 “fixed 01s”). If the swap remains in place until maturity, and the end user is appropriately applying hedge accounting, the impact of this change is largely irrelevant. However, for those end users not applying hedging accounting or who anticipate terminating the swap prior to maturity, the impact of this change is quite real. In general, the magnitude of the impact of this change in discounting is positively correlated with both the tenor of the swap and the amount by which the swap is in or out of the money.

Figure 3: Cashflows for a hypothetical swap under which end user pays a fixed rate of 5.25% and receives 1 Month LIBOR over the next 25 years on $100 million (non-amortizing). Fixed and variable cashflows are based on an Act/360 daycount. Monthly discount factors have been aggregated for brevity. Data source: Bloomberg

For new swaps, the impact may not be as evident. In a perfectly flat yield curve environment where the fixed rate is equal to the anticipated forwards along the entire term curve, there would be no impact of changing the discount rate (there are no anticipated “net” cashflows to discount). However, swap dealers require compensation to cover credit exposure, hedging costs, and profit. As the swap rate is altered the swap immediately becomes a liability for the end user and larger so using OIS discounting. So even with a flat yield curve, the value of the swap is impacted (albeit moderately so).

In today’s market where the yield curve is upward sloping, the impact is more noticeable. Figure 4 shows 1M LIBOR forwards versus the mid-market 10 year LIBOR swap rate. We can see that because of the steepness of the current yield curve, the positive cashflows – for the fixed rate receiver – are expected to occur within the first 4.5 years while the negative cashflows – for the fixed rate receiver – occur between year 4.5 and year 10 (i.e. – the negative cashflows are being discounted for a much longer period). By using the lower OIS discount rate, the positive cashflows are only slightly more positive while the negative cashflows are much more negative than if we had used a discount rate based on the 3 Month LIBOR curve. To offset this discrepancy, the fixed rate on the swap must be increased so that the present value of the positive cashflows offsets the present value of the negative cashflows. In short, OIS discounting will increase fixed swap rates in today’s market. In the case of a ten year swap, the fixed rate must be increased by approximately 1 basis point (0.01%).

Figure4: 1 Month LIBOR forwards versus current 10 year fixed swap rate. The swap rate assumes a floating index of 1 Month LIBOR, paid monthly, Act/360 daycount.

The impact of higher fixed swap rates will also have a direct impact on option strategies including caps, floors, and swaptions. Not only will the “at-the-money forward rate” be higher in today’s environment, but the premium generated by options will be discounted at a lower interest rate.

What Can End Users Do?

End users should discuss swap dealers’ discounting methodology prior to entering into any new swap transactions. This should include a discussion as to how they’re currently discounting swap cashflows as well as how they anticipate doing so in the event the swap is terminated in the future. For those that have existing swaps in place that will be adversely affected by OIS discounting, the jury is still out.

It has been our experience that a few end users desiring to terminate swaps in the near future are trying to get their swaps “grandfathered” under the prior discounting methodology if they terminate in the very near future. Depending upon an end user’s cash reserves and rate view, terminating could be an option. For our end user above with their $100 million 25 year swap, terminating today using 3 Month LIBOR discounting versus terminating tomorrow using OIS discounting would save them over $1 million. For those end users that anticipate carrying swaps to maturity and are applying hedge accounting, there may be no cause for alarm to begin with. Regardless of the outcome, we feel that this unilateral change to a decades-old methodology is sure to be a topic of debate in the near future.